The findings of 377 Union reported on February 20, 2017 in Who is Steve Calk, and what does he have to gain from helping Paul Manafort? were subsequently picked up by The Intercept, WNYC, and The Wall Street Journal.

When reached for comment, Calk indicated that the loans were “grossly overcollateralized.” Manafort’s response was that “As is standard, the loan amount is based on the appraised value of the property after renovation, not the value of the property as-is.” Note that Calk’s response focuses on the total collateral, and Manafort’s response focuses on the potential post-renovation value of the underlying real estate asset.

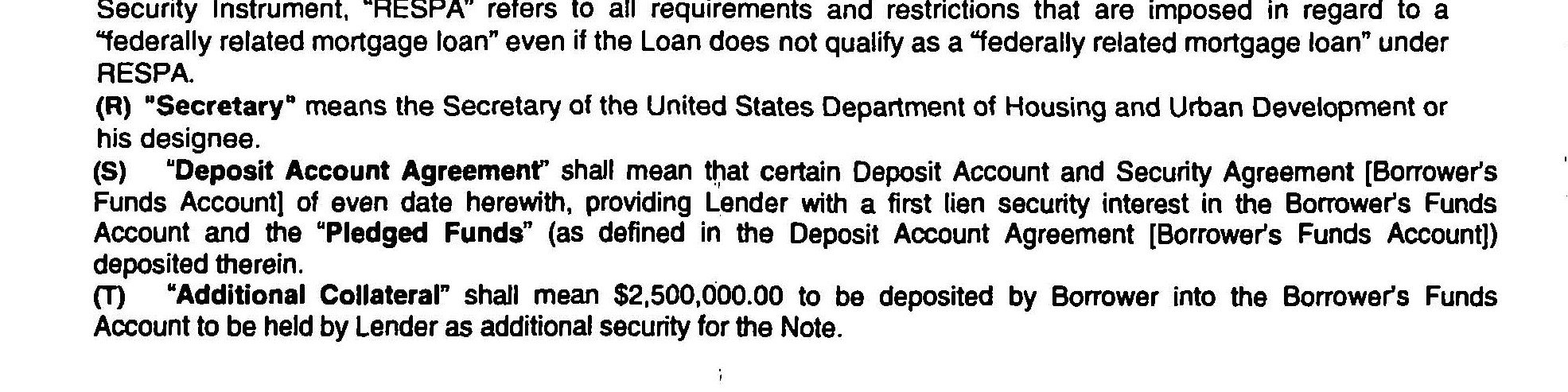

Indeed, the two loans from The Federal Savings Bank included a requirement that Manafort pledge certain cash assets as additional collateral. Specifically, Manafort was required to pledge (i) $2.5 million for the loan secured by the Union Street property and (ii) $630,000 for the loan secured by the Bridgehampton property.

Collateral may have been an important detail in a 2004 BB&T loan to Manafort described in another post on this site (see “The Wellington Farm”). In 2004, Manafort borrowed $2.8 million on the Alexandria property which was sold in 2015 for only $1.4 million. As with the 377 Union Street loan, the size of the loan in comparison to the value of the property (implied by the sale price) raises two questions:

(i) How would a lender ensure that they have sufficient pledged collateral in such a situation?

(ii) Why would someone take out a loan on a property that exceeds the property’s potential value?

It makes sense from the lender’s perspective to require additional collateral (in the case of 377 Union Street, in the form of cash) on an otherwise risky loan (i.e. a loan for arguably more than the value of the underlying security interest and to a borrower already in default). But what about from the borrower’s perspective?

If a borrower has full and uncompromised access to $3.13 million (the amount of cash collateral pledged to The Federal Savings Bank) in cash available for collateral, why not simply use that cash, decrease borrowing by an equivalent amount and save on interest payments and other fees? In the Manafort/Calk case, the interest rate is apparently above market (7.25%), only making this arrangement even more puzzling/penalizing for the borrower…

Please contact us with any comments.